ServiceNow (NOW)

Widespread Mistakes in Analyst Share Counts Fuel Overvaluation

Disclosure

We are short shares of NOW. Please click here to read full disclosures.

It’s certainly been a year to remember for investors, with the benchmark S&P 500 up 30%, the tech-heavy NASDAQ-100 up 37%, and many sectors, including cloud computing, rising further yet. Last year provided great opportunities to make money, as every dip in the market has been an excellent buying opportunity.

But the tech euphoria has gotten out of hand in certain sectors. In many ways, the investing community seems to be repeating its mistakes from the irrational exuberance of the late 1990s. Many investors are buying stocks not due to fundamentals, but rather due to sexy-sounding stories of future growth combined with momentum: as in that previous internet tech era, people are again buying stocks principally because the stocks are already rising and have garnered investor enthusiasm.

In the case of ServiceNow (NOW), we’ve already discussed the very low likelihood that the company can grow into its valuation. Longs are overestimating ServiceNow’s addressable markets and software capabilities. Investors were shown another red flag last Thursday when NOW’s Chief Technology Officer, Arne Josefsberg, who joined the business in October 2011 after 25 years with Microsoft, unexpectedly resigned from his position.

But enough has been said about ServiceNow’s business prospects. We’d rather focus on the more basic similarities between the current environment and 1999. One of the most jarring flashbacks has been the return of extremely sloppy and dubious sell-side research. While we have not quite hit the excesses of the tech bubble yet, we’re seeing disturbing reminders of that past mania.

During the 1990s tech boom, abuses within equity research led to SEC enforcement actions, industry bans and a litany of new regulations to curtail the regular exchange of stock promotion for investment banking business. Reg FD was enacted in 2000, Henry Blodget was banned from the industry and “Chinese Walls” sprang up all over the industry.

Ten years later, it appears that history is repeating itself. With the IPO and secondary offering markets as hot as they’ve been in ages, it seems that banks may again be putting deal-making ahead of quality research.

In the specific case of ServiceNow, analysts have gotten sloppy on one of the most basic inputs of equity valuation: the number of fully diluted shares of common stock. Visit a basic finance website such as Yahoo Finance or Google and you’ll see 138.7 million shares for ServiceNow, leading to a market cap of about $8.1bn at the current $58 share price. You could forgive an ordinary retail investor for assuming that this information is accurate.

However, professional investors should always be aware of the total capital structure, rather than just the number of current outstanding shares, which is one of many inputs to determine valuation. In the case of young companies, particularly in technology, analysts can’t overlook stock option grants to employees. Since tech startups tend to be short on cash and long on blue sky potential, they forgo paying higher compensation in the short-run and defer it via options. Usually this doesn’t make too much of a difference in the long run, but if a company is particularly successful, and/or its shares perform exceedingly well, the impact of options grants given to executives and early-hire employees can be dramatic.

ServiceNow has more than 25 million outstanding in-the-money stock options, in addition to almost 5 million restricted stock units (“RSUs”) (2013 10-Q3). With the options having an average strike price of $8.12 and RSUs providing no future cash to ServiceNow’s treasury at all, these 30 million issued shares represent a tremendous dilutive overhang to the company’s share count. When these 30 million shares convert into common stock, the company will raise only ~$200 million in proceeds but be burdened with $1.75bn of newly traded common stock.

In reality there are 169 million shares of ServiceNow, or 165.4 million using the treasury stock method, rather than the 139 million you see reported at sites such as Yahoo or Google. And it’s excusable that these free finance sites are wrong; you get what you pay for. This is why an investor should always check a company’s filings rather than simply trusting a free website’s computer-generated financial information.

It’s less excusable when professional equity research analysts, trained at top business schools and working at prestigious investment banks, are no more reliable than Yahoo Finance. We first noted a year ago that several bulge bracket analysts were overlooking the option pool. We figured that analysts would quickly correct what we figured was merely a simple oversight.

But it’s now been more than a year, and analysts are still willingly sticking with their clearly inaccurate numbers. Numerous banks continue to mislead clients with wildly inaccurate share counts and market capitalizations for ServiceNow.

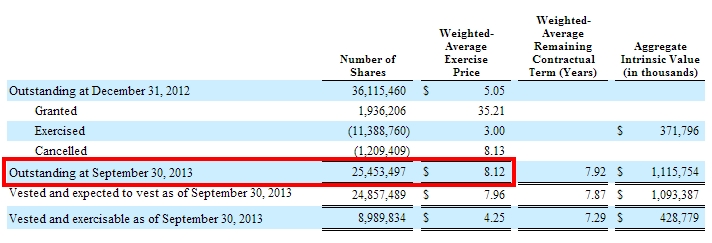

Data to calculate the correct share count is easily found in ServiceNow’s latest 10Q-3 2013:

Here, we see 138.7 million shares of common stock, 4.8 million Restricted Stock Units (RSUs), and 25.5 million outstanding stock options. RSUs cost employees nothing to exercise, so those are virtually assured to turn into common stock as they vest. Now let’s check the outstanding options to see where their strike price is on average:

Given that the average exercise price for the options is $8, compared to a current share price of $58, and even the most recently granted round of options are still well in the money, it should be assumed that the vast majority of these options will turn into common stock as well. Thus, adding together the 138.7 million common shares, the 4.8 million RSUs, and 21.9 million dilutive impact from the options (using the treasury method), we arrive at 165.4 million fully diluted outstanding shares, which results in a market cap of $9.6bn. Not so difficult.

By comparison, below is a quick tour around various investment banks’ reports for the company. These figures were pulled from the batch of October 23-24th reports following NOW’s Q3 2013 results.

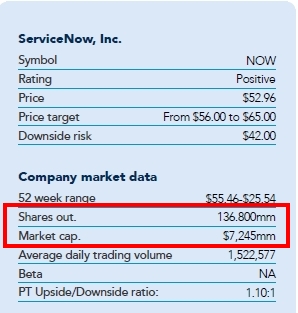

Wells Fargo:

Wells Fargo claims 137.5 million shares. Did they simply lift this figure from Reuters?

Barclays:

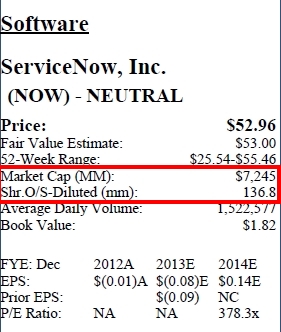

Barclays claims 136.8 million shares. At least Barclays can blame FactSet Fundamentals for getting it wrong, perhaps?

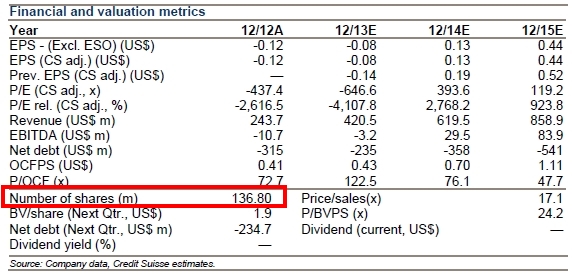

Credit Suisse:

Credit Suisse follows Barclays’ lead with a similarly erroneous 136.8 million figure.

Deutsche Bank:

Deutsche Bank diverges from the others using a share count of 147 million (still well off the correct figure) to arrive at its mistaken market cap, which they make sure to provide in both dollars and Euros.

Susquehanna:

Susquehanna follows the example of several other firms that really like that 136.8 million share count figure.

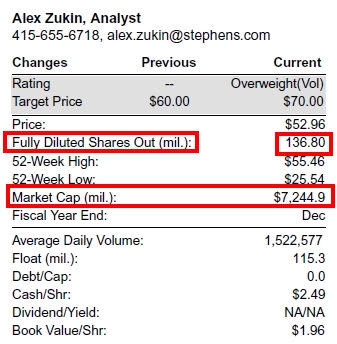

Stephens:

Notice that Stephens specifically characterizes its share count as “fully diluted”. Not only does Stephens attach itself to the inaccurate 136.8 million figure, but by including the words “fully diluted,” Stephens earns itself a special spot within the ServiceNow equity research hall of shame.

Janney:

Janney, not bucking consensus, uses the faulty 136.8 million figure as well.

The preceding reports were prepared before the release of NOW’s 10-Q3 2013 on November 4th. Yet this does not excuse the oversight of the option pool. As of 10-Q2, NOW still had 136.8 million common shares, 27.5 million options with an average strike price of $7.16, and 3.9 million RSUs. At a $52.96 share price, this would equate to 164.5 fully diluted million shares, still nowhere near the figures cited in the brokerage reports.

Furthermore, the justification that options are “anti-dilutive” given NOW’s ongoing net income losses is ridiculous. Option grants are not free, nor does the conversion right disappear, just because a business isn’t profitable.

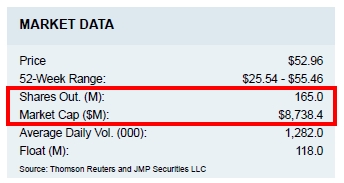

We also want to be clear that there are a handful of firms that do list the correct share count for ServiceNow. In contrast with all the erroneous tables above, here is a table from JMP Securities, for example, whose analysts actually did their math properly and account for the upcoming new shares:

Bravo JMP! For correctly calculating something as basic as shares outstanding!

It is important to note that investment banking analysts normally are capable of determining the correct number of shares outstanding in a company’s stock. It’s perplexing that the majority of the Street won’t or can’t get the number right here. It truly is unusual to see so many firms be this wrong about something this basic and remain mistaken for such a long period of time. By contrast, check out the below November 19th, 2013 price target upgrade from Citigroup’s Yaron Werber:

Werber digs far enough into the weeds to calculate that a previously dilutive convertible note/warrant package is being retired prematurely, and as such, the consensus view of the outstanding share count is too high. Not only had the Street (correctly) factored in a previously announced potential dilutive overhang, but now an analyst realized the overhang will have been cleared and in turn adjusted the price target accordingly. This is the sort of analysis we expect from professional investment analysts, which makes the grossly misleading ServiceNow coverage all the more ludicrous.

Why are the Analysts so Wrong?

The bigger question may indeed be why analysts are unable or unwilling to factor in 27 million shares, or $1.55bn worth of capitalization, of way-in-the-money soon-to-be common stock. Previously, you could have ascribed the error to mere sloppiness. Perhaps everyone was pulling their numbers from Yahoo Finance or otherwise not digging into the SEC filings enough to pull out the real number of outstanding shares.

But since we launched our coverage on ServiceNow more than a year ago and highlighted the fact that the majority of analysts were using grossly inaccurate share counts, it seems harder to attribute the misstatement to mere sloppiness at this late date. A simple oversight like that, once pointed out, is easy to correct.

In theory, there is a so-called “Chinese wall” between the parts of investment banks that analyze companies and the parts of investment banks that earn fees from companies by providing them services such as IPO and secondary underwriting advisory. In practice, however, it is often questionable whether or not there is much separation between the research and banking arms of financial firms.

Take, for example, the recent Evoke Pharma IPO (EVOK). Aegis Capital was the sole bookrunner for the Evoke IPO, no doubt earning a healthy fee for its services. Earlier this month, following the IPO, Aegis’ biotech analyst launched coverage for Evoke, then trading at $8, with a jaw-dropping $60 price target. Needless to say, a 650% upside target raises eyebrows, and the more conspiratorially-minded person might draw a connection between Aegis’ ambitious price target and Aegis’ earning of Evoke’s IPO fees. Any company considering Aegis’ IPO services in the future will likely recall the underwriter’s most favorable research opinions for IPOs it has recently underwritten. If you were seeking to define the phrases “perverse incentive” or “moral hazard” in a business textbook, this sort of example would come to mind.

Historically, the “wall” between investment research and banking has often resembled clear cellophane as opposed to anything reliably separating the two divisions. During the last tech boom, CEOs were openly telling analysts to raise their investment ratings before they’d consider doing banking business with the analyst’s firm. For example, Bernie Ebbers, former CEO of MCI WorldCom, was asked if he’d do a banking deal with Merrill Lynch. Ebbers replied, “No. We have to have a better rating before Merrill Lynch would do the investment banking.” This doling out of banking fees based on investment research ratings was common practice, as former telecoms analyst Dan Reingold, in his book, recounted: “Bernie [Ebbers] wasn’t one to mince words. He simply said aloud what others thought to themselves.”

Later on during the cycle, Jack Grubman, Soloman Smith Barney’s former rock star telecom analyst, was asked by Soloman’s president to “take a fresh look” at his long-standing negative opinion on AT&T. Grubman soon upgraded AT&T shares. Seemingly as a result, Soloman reaped lucrative fees from a deal involving an AT&T wireless subsidiary spin-off. Grubman, for doing his part to generate banking business, was able to leverage his upgrade to get his employer to donate $1 million to the 92nd Street Y so that Grubman could get his children accepted into an exclusive Manhattan nursery school.

After examples like this, it’s no wonder that market participants began to have doubts about the independence of Wall Street research. Former New York Attorney General Eliot Spitzer confirmed people’s worst fears when his investigation hit the mother lode of wrongdoing at Merrill. Among internal emails at Merrill relating to Goto.com, a stock they had a “buy” rating on, Spitzer found one where an investor emailed Merrill about the company: “What’s so interesting about GOTO except banking fees????” A Merrill research analyst replied: “nothin.” Or from one Merrill analyst to another: “I don’t want to be a whore for f–ing management. We are losing people money and I don’t like it. john and mary smith are losing their retirement because we don’t want [the CEO of Goto.com] to be mad at us.” In another example, former Merrill analyst Henry Blodget referred to a stock he had a buy rating on as a “piece of shit” in an internal e-mail.

Despite all the talk of a wall between investment research and banking fees, it’s clear where Wall Street’s biases lie. Which brings us back to ServiceNow, as NOW has been a most prodigious generator of banking fees itself. A cynical person might suspect that ServiceNow’s propensity to unceasingly emit new stock and debt, and in the process offer lucrative fees to investment bankers, is in some way tempting analysts to look for the bright side of ServiceNow’s rather cloudy forward business prospects.

Hypothetically, one great way for analysts to juice up their analysis and be able to have their models spit out more optimistic price targets would be to undercount, inadvertently or intentionally, the number of outstanding shares. For ServiceNow, by ignoring the existence of 27 million fully diluted shares, analysts have an extra $1.55bn of breathing room to use when constructing their valuation estimates.

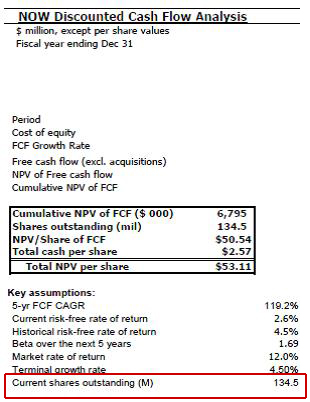

For a look at this in action, consider Janney’s valuation model from its October 7th Initiating Coverage report for ServiceNow:

Janney employs a discounted cash flow analysis model. Their model assumes optimistic growth rates of free cash flow, rising from $8 million this year to $74 million by 2015, $339 million in 2017, and all the way up to more than $1.6 billion by 2022. Obviously, it seems a little ridiculous to forecast a 132% compound growth rate of cash generation over the next five years when in fact ServiceNow’s free cash flow generation has been virtually nil over the past several years and has shown little sign of turning the corner in recent quarters.

But even granting this most optimistic of forecasts, Janney’s model still only deduces a net present value of $53.11 per share ($6.8bn of net present value plus cash). This doesn’t seem bad (or particularly good) given that the stock is trading at $58. But when you realize that Janney only accounted for 134 million shares, contrasted with the 165.4 million actual fully diluted shares of ServiceNow, you have to re-run the math. Dividing that $6.8bn of net present value plus the cash balance of $347m by 165.4 million fully diluted shares, you see that Janney’s real price target is near $43! Even if ServiceNow manages to meet Janney’s lofty operating growth targets, the stock is still overvalued by 25% at present levels!

And Janney is far from the most optimistic of analysts on the street. Other more bullish firms have much more outlandish price targets. For ServiceNow, which generates almost no cash and loses money on a net income basis despite having conquered close to a quarter of the market share in its rather limited addressable market (particularly since peak penetration is likely only around 50% given security concerns around using a cloud-based service for sensitive data), it’s hard to fathom what sort of upside analysts are fantasizing about.

How It’s All Going To End

ServiceNow has a reasonably good ITSM product, and it will likely continue gaining share in that market. From its current 30% market share (Gartner estimates market size near $1.5bn), NOW could, with good operating performance, get to maybe 50% market share as more clients move from BMC’s legacy solutions to ServiceNow’s cloud offering.

The touted great upside of the IT operations and PaaS is simply unlikely to occur. Analysts are hyper-focused on the platform area because ServiceNow’s current operations cannot come close to justifying the company’s daunting $9.6bn market cap. We don’t believe the platform business is sufficiently promising to justify the sky-high valuation multiples.

ServiceNow insiders have been dumping shares, issuing dilutive financings, and waiving lock-up commitments for IPO shares in order to, it seems, squeeze as much cash as possible out of its overinflated share price. Wall Street analysts complacently keep offering up fanciful research opinions including a basic $1.6bn misstatement of ServiceNow’s market cap, while the banking teams keep collecting fees off ServiceNow’s latest public offerings. Needless to say, this probably won’t end well for investors late to the party.

Add New Comment