Disclosure

We are short shares of MLNX. Please click here to read full disclosures.

Mellanox (MLNX), a stock that we’ve previously written up as a short recommendation, announced disappointing Q4 2012 results yesterday and gave catastrophic Q1 2013 revenue guidance. Though the stock initially dropped 22% after hours to $41, MLNX shares eventually rallied to $51 signifying a mere 1.4% decline for the day. Given three quarters of massive revenue declines ($157m in Q3 2012, $122m in Q4 2012, and ~$80m for Q1 2013) this is a stock that should be trading at a much lower level. With analysts having issued downgrades en masse and no longer supporting the stock with blind optimism, MLNX should reverse its intraday gains and fall to the $30s.

Valuation Remains Much Too High

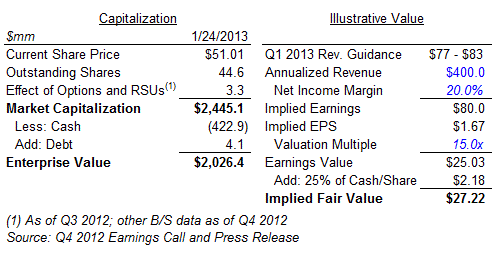

Today at $51, shares of MLNX remain highly overvalued.

First, Mellanox clearly no longer deserves a premium valuation multiple. Business fundamentals have been suffering a steep decline over the past few quarters. The company’s Q1 2013 revenue guidance of $77 – $83m is well below the $89m of revenue made in the first quarter of last year. The forecast represents a 34% decline from the fourth quarter, and missed analyst estimates of $130m by a stunning 40%. As we summarize later in this article, the company’s 2012 growth was the product of the Intel Romley upgrade cycle, and with the cycle having now turned, investors are reminded that Mellanox is simply yet another cyclical semiconductor company. As a result, we assume a 15x earnings multiple, comparable to the multiples of a peer group of Emulex (ELX), Brocade (BRCD), and QLogic (QLGC). These analogous interconnect businesses have modest growth expectations, as MLNX investors should come to expect, and somewhat commoditized product offerings, which high-speed Infiniband will soon become.

We will discuss later in this article why even this 15x earnings multiple is highly optimistic, since there is a strong chance that MLNX’s high-end Infiiniband business will be rendered extinct by Intel (INTC) within the next five years.

Having determined an appropriate multiple, let’s next examine Mellanox’s 2013 figures. Management has not provided guidance beyond next quarter, and analysts have yet to digest the company’s stunning 40% revenue miss and issue new estimates, so we’ll make some basic assumptions. If we optimistically assume that Mellanox actually meets its quarterly guidance for the first time in over six months, then the company would earn an annualized $320m in revenue in Q1. Let’s assume some growth in subsequent quarters and therefore 2013 revenue of $400m. At a 20% net income margin (Q4 2012 was only 15% on a GAAP basis and historical years prior to 2012 witnessed profit margins under 10%), the company would report earnings per share of about $1.70. At our 15x P/E multiple, generous in light of the potentially terminal nature of MLNX’s business, we’d assign $26/share of value to the earnings stream. The company holds $9/share of net cash, but smallcap semiconductor companies have a poor history of returning cash to shareholders and MLNX has never paid a dividend or repurchased shares, so we only give credit to 25% of that cash.

Adding $2/share of net cash to $26/share of business value and rounding up gets us to a fair value of about $30/share, a 40% discount to the current price. Below is a table summarizing our calculations.

(click to enlarge)

Yet even at $30, owning MLNX shares remains highly risky. That’s because there’s a good chance that Intel’s next-generation CPU+Interconnect design will render MLNX extinct within 5 years. As such, we took the opportunity to materially increase our short position after yesterday’s irrational intraday short covering rally. Below is an intraday graph of yesterday’s price action:

(click to enlarge)

Source: Yahoo Finance, January 24th, 2013.

The Stock has Lost the Support of the Sellside

After its surprisingly strong growth in the first half of 2012, analysts rushed to outdo one another with $140-$150 price targets and ebullient Buy recommendations. Since most analyst models simply projected quarterly revenue using straight-line growth assumptions, infectious optimism quickly enveloped this momentum stock. Even at its peak price near $120 on September 6, MLNX was awarded Buy ratings by the majority of the analyst community and price targets were dutifully increased as the stock ticked upwards. Below are Bloomberg analyst ratings from September 6.

(click to enlarge)

Source: Bloomberg Analyst Ratings, September 6, 2012.

Times have changed. After Wednesday’s Q4 2012 earnings call, many analysts finally recognized their folly. What was once a sea of green ‘Buys’ is now overwhelmed by ‘Holds’, which is actually a code word for ‘Sell’ on Wall Street.

(click to enlarge)

Source: Bloomberg Analyst Ratings, January 24, 2013.

The once flowery praise has been replaced with scorn:

“Further exacerbating the impact of weak guidance, management’s tone and demeanor was off-putting and at times seemingly evasive as it “stonewalled” analyst attempts to garner additional color into specific details surrounding the weak guidance…we believe management has significant work ahead to restore investor confidence.”

– Wunderlich Securities “Stunned, Stonewalled, and Sandbagged,” January 24th, 2013

“We thought we’d seen everything, but apparently we hadn’t…The guidance for the first quarter of 2013 is catastrophic – $78-83 million… the company has almost no control over demand or influence on OEM customers to buy from it…There is no question that rebuilding capital market confidence will be protracted and arduous.” – DS Brokerage, January 24th, 2013

The white-shoe investment banks were more gentle about their disappointment, but the overall tone was negative nonetheless:

“We are lowering our TP to $40.00 from $55.00…we believe the market needs to see a path back to $150m/quarter run-rate before any meaningful appreciation in stock price – hence, we remain Neutral.”

– Credit Suisse “Growth Hibernates for the Winter,” January 24th, 2013

“Given the sell-off from the peak, negative sentiment, and our anecdotal sense that many investors appear to have moved to the sidelines, we expect the shares to settle in the $40s with support from the ~$10/share in cash.”

– Barclays “Resetting the bar,” January 24th, 2013

Once a company loses the confidence of the sellside, it usually becomes much more difficult to win back. Analysts won’t want to risk their reputations on a stock that has already burned them once before.

Will Mellanox Be Around in Five Years?

During the September 11-13th Intel Developer Forum, Intel officially announced its intention to integrate its next-generation CPU with an interconnect device, theoretically cutting out the need for a third-party interconnect provider like Mellanox. Intel’s intent was mentioned by multiple press sources and presentations from Intel’s technical sessions on the topic are available online. By assembling interconnect technologies and engineering teams from Cray, QLogic, and Fulcrum, Intel should be well positioned to complete its task. But even if Intel doesn’t meet its timeline goals, the chipmaker controls the CPU design, allowing it to build a design that only functions optimally with an Intel’s interconnect. This integration could potentially provide power and performance synergies as well as cost savings for the end-users. It would also completely box Mellanox out of the high-end HPC (high-performance computing) market.

(click to enlarge) Source: Intel Developer Forum, Diane Bryant, September 11th, 2012

Source: Intel Developer Forum, Diane Bryant, September 11th, 2012

When asked about this threat from Intel in the third quarter conference call, the Mellanox CEO essentially had no viable solution, admitting that Mellanox would have no choice but to “find the right way to work with them or to compete with them”. In other words, Mellanox has little influence on whether Intel will render the company’s products obsolete.

The full discussion from the call is below:

<Dan Harverd, Deutsche Bank AG, Research Division>

And then just a final question, a longer-term question. We’ve seen Intel during the quarter for that roadmap for its plans and InfiniBand, and potentially interconnect control into CPU. Could I get any thoughts on that and how that would affect your business going forward?

<Eyal Waldman, MLNX Executive Chairman, CEO, and President>

Obviously, we are working with Intel in multiple dimensions. Intel will try to come out something in the 2015, ’16 time frame with their 100 Gigabit per second solution. It’s yet to be seen how we work together if we work together at that time frame. And obviously, Mellanox, we continue to develop our own solutions for the 100 Gigabit per second, which we think will come out in 2014 time frame, so we still hope to continue leading this market and keep taking market share away from our competitors.

<Dan Harverd, Deutsche Bank AG, Research Division>

And if they were to come up with an integrated product, would that change — how would you see that changing the fundamentals of the market?

<Eyal Waldman, MLNX Executive Chairman, CEO, and President>

Well, then we’ll find the right way to work with them or to compete with them.

If Intel builds an interconnect solution into its next generation of high performance computing CPUs, there probably is no “right way” for Mellanox to work with them or compete with them.

Why Mellanox no Longer Deserves a Premium Multiple

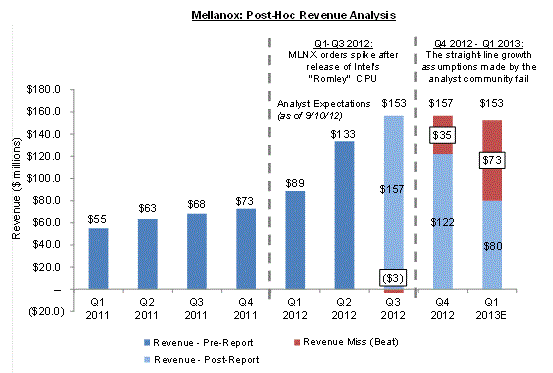

Our initial report on September 10th, 2012 questioned the Street’s overly simplistic growth assumptions and probed for more concrete answers to explain the company’s rapid good fortune. Based on our research, Mellanox’s growth was attributed to high-performance computing customers who were paying up for the premium priced 56GB/s FDR Infiniband in order to fully utilize newly installed Intel “Romley” CPUs. We felt that this Romley uptake cycle would soon wane and predicted that the straight-line revenue assumptions for Q4 2012 and early 2013 were flawed.

After the third quarter earnings call, MLNX’s CEO mentioned “a revenue baseline of $150 million,” a figure that was quickly latched onto by analysts hoping to construct their two-year models. On the same call, the CEO also warned, “you know again, we don’t give guidance or visibility more than one quarter” yet appeared to acquiesce when analysts inferred that $600m would become the annual revenue baseline and the de facto worst case scenario for the Street’s models. Investors continued to trust the company even after the management gave underwhelming Q4 guidance on their October 17th third quarter call. Q4 revenues were projected at only $145m – $150m, implying a sequential decline in revenue of 6% that was well below growth expectations. Those who followed the story closely noticed a second chink in the armor when the newly installed CFO revealed MLNX’s complete lack of end-market visibility at a November 14th UBS conference, stating, “we said that $150 million is a baseline. That’s purely based on our gut feeling [Emphasis added].”

After that comment, we were stunned that the analyst community continued to take guidance from management at face value. In contrast to the analyst expectations of September 2012, when $150m of run-rate quarterly revenue was considered the floor and consistent sequential growth was the expectation, it’s clear that MLNX’s ephemeral revenue boost was the result of the Romley uptake cycle and not a sustainable trend.

(click to enlarge)

Source: Capital IQ, MLNX earnings calls and filings (10K, Q4 2012 8K).

Our chart from the September 2012 report shows that the revenue shortfall has essentially matched the predicted demand from the Intel server ramp cycle.

(click to enlarge)

Source: Jefferies Research note on IPHI, February 1st, 2012.

Given this relatively straightforward explanation for the recent revenue shortfall, we believe that the guidance for Q1 2013 is more indicative of what revenue will look like throughout this year. This should be exacerbated by the increased uptake of 40GB/s Ethernet, which has a much lower price point than 56GB/s Infiniband.

Broadcom (BRCM), a leader in 40GB/s Ethernet, explained this during a Deutsche Bank conference in September:

“And [the HPC] market, as you know, there’s a natural transition happening in speeds, going to 56 Gb Infiniband as the Romley cycle comes on…And that’s been [MLNX’s] traditional market. There’s been some adoption of Infiniband in other markets, right. Also, they talked about a large cloud customer, and they also talked about some increasing need for storage cluster for the back end. And if you look at those markets, for the most part it’s a pricing game and a density game between Ethernet and Infiniband, right? So today, we have 56 Gb Infiniband in the market…And now with Trident II — by the way, 40 Gb Ethernet is going to start shipping and going after exactly the same market that they’re in right now. Now the end customers have a choice, right. They can go buy…from Mellanox, or they can go buy 40 Gb Ethernet switches that do essentially the same thing from 10 different providers, with an open ecosystem and standards-based interoperability that they don’t have to worry about. So to me…[Ethernet providers are] going to be in a good position to go back out there and make sure that all the business that’s on Ethernet remains on Ethernet versus going to Infiniband.”

We think that this rapid influx of 40GB/s Ethernet into the much more cost-conscience Web 2.0, cloud, and storage markets will prevent MLNX from growing meaningful beyond their HPC customer base.

Conclusion

Ultimately, Mellanox is a company with dramatically declining 2013 revenue and profitability, a management team that has lost credibility with the sellside, and a core product line that may be rendered obsolete by Intel. It does not deserve a 6x forward revenue multiple or 30x P/E multiple. Having lost its growth / momentum investor base due to large earnings misses and rapidly declining investor sentiment, the current inflated stock price is mostly the product of yesterday’s short covering rally. Such rallies are often fleeting, and MLNX shares could soon resume their steady descent.

DISCLAIMER: WE ARE SHORT MLNX AND BENEFIT TO THE EXTENT THE PRICE DECLINES. THIS IS NOT A RECOMMENDATION TO BUY OR SELL SECURITIES. WE MAY TRANSACT IN SHARES OF MLNX SUBSEQUENT TO PUBLICATION.

Add New Comment